- Find a Brokerage Firm

- Find a Listed Company

- Contact Us

- Connect PSX

Published by: Pakistan Stock Exchange

Pakistan Stock Exchange (PSX) is launching Cash-Settled Futures (CSF), giving investors a simpler way to take a view on future share prices without worrying about the physical delivery of shares. In this market, investors enter into a contract today based on their expectations about where a share’s price will be in the future and, at the end, only the difference in price is paid or received in cash, along with the daily Mark-to-Market (MtM) settlement.

In a CSF contract, an investor agrees to buy or sell eligible shares at a future date at an agreed “futures price”. There is no exchange of the actual shares against complete transaction amount at expiry . Instead, on the last day, the contract is settled in cash: the futures price is compared with the final settlement price (the closing price in the Ready market), and the difference is credited or debited to the investor’s account.

For example, if the CSF Futures price was Rs 150 and, at expiry, the underlying share closes at Rs 160, the buyer receives Rs 10 / share in cash from seller (or Rs 5,000 = 10 x 500, as each contract represents 500 shares). If the price closes below Rs 150, the seller gains and loss is paid by buyer in cash instead.

The CSF market has been designed to be lighter on capital and smoother in operations. First, settlement is purely in cash, which reduces the operational and settlement risks linked with arranging physical delivery of shares.

Second, CSF uses the globally recognized Ratio-based method to handle corporate actions (such as dividends, bonus and right issues). Instead of breaking contracts into A and B series, contract prices and contract multipliers are adjusted so that the investor’s overall exposure remains broadly the same before and after the corporate action event (excluding any tax effects).

Third, Unlike DFC, the MtM profit is fully distributed to the account holder by NCCPL on T+1, which account holder can withdraw completely.

Moreover, the basic deposit requirement has been completely waived off for brokers, compared to PKR 1 million required by brokers to trade in Deliverable Futures Market. In addition, there CSF market is given a trading fee holiday for initial three months by Pakistan Stock Exchange and National Clearing Company of Pakistan i.e., these institutions will not charge any trading fee in CSF market for initial three months.

All types of investors – individual, institutional, local or foreign are allowed to trade in the CSF market through their brokers, subject to usual account opening, KYC and risk-profiling requirements.

Initially, 82 stocks have qualified the CSF eligibility criteria. These include many well-known names from banking, cement, energy, fertilizer, technology and other sectors. List of these tradable stocks under CSF is readily available on PSX website and social media channels. The eligibility list is reviewed every quarter against the quantitative and qualitative thresholds set in the Criteria.

Each standard CSF contract currently represents 500 shares of the underlying stock, known as the “contract multiplier”. This multiplier may be adjusted if there is a corporate action, but the idea of a fixed block of shares per contract remains the same.

At any time, investors can trade CSF contracts with three maturities – roughly one-month, two-months and three-months contract. New contracts are listed on the first trading day after the last Friday of each month, and the current month’s contract expires on the last Friday of its calendar month.

The investment needed is much lower than buying the same number of shares in the Ready market. For instance, buying 500 shares of a company at Rs 200 in the ready market requires Rs 100,000. Taking exposure to the same 500 shares via CSF, with an assumed margin requirement of 10%, would require only Rs 10,000. The investor still gains or loses on the full 500-shares exposure, but only a fraction of that value is paid upfront as margin.

This margin system introduces “leverage”. Because only part of the contract value is deposited, any change in price results in a larger percentage gain – or loss – on the investor’s own money.

For example, if an investor uses Rs 100,000 to buy shares in the Ready market and the price rises from Rs. 200 per share to 240, the gain is Rs 20,000 or 20%. In a leveraged CSF position on the same underlying, the same Rs 100,000 could provide a much larger exposure for instance a maximum of 10 times due to 10% margin requirement, so a similar move in the share price could lead to a significantly higher percentage profit, in example 10x i.e., Rs. 100,000 or 100%. But the reverse is also true: a relatively small adverse move in price can quickly eat up the margin and trigger losses. Hence, if it has a potential to magnify the profits, it can also magnify the losses in adverse movement.

For this reason, CSF should be used in a systematic manner with clearly understanding the rules of the product to avoid or minimize adverse market movements.

CSF positions are “marked to market” every trading day. The Exchange calculates a Daily Settlement Price for each contract, usually based on trading price in the CSF market and considered aligned with underlying spot price. Positions are revalued at this price each day.

If an investor is in profit for the day, that amount is credited in cash on the next day. If there is a loss, it is collected in cash. At expiry, a final settlement is made using the Ready-market closing price of the underlying shares against the futures price, and the contract is closed.

This daily settlement system ensures that gains and losses are realized gradually, and helps the clearing company manage risk across the market.

Dividends, bonus shares and rights issues are a fact of life in the stock market. In the DFC market, such events often meant splitting contracts by creating A and B series. Under CSF, the approach is more investor-friendly. When a corporate action is announced and the share price goes ex-dividend, ex-bonus or ex-right, PSX and the clearing company adjusts both the futures price and the contract multiplier using a defined formula. The aim is to keep the overall exposure of the investor approximately the same before and after the corporate action adjustment (excluding tax impact), and any small difference due to rounding-off impact will be adjusted by NCCPL. This means investors can hold their CSF positions through corporate actions without worrying about managing multiple series, which is a key improvement over DFC.

There are several practical ways in which investors can use CSF:

The relaunch of Cash-Settled Futures at PSX is an important step in deepening Pakistan’s derivatives market. It has taken into account investors input and expectation while designing the product in line with international benchmarks. It gives investors a tool to trade, hedge and manage risk with lower capital requirement, no physical delivery and a more transparent settlement process. As with all leveraged products, CSF requires understanding and caution, but used wisely, it can become a valuable part of the toolkit for both individual and institutional investors.

Disclaimer: “Investments in the Stock Market are subject to market risks. The prices of securities may go up or down depending upon the factors and forces affecting the securities market. The past performance of any security is not necessarily indicative of its future performance. Investors are requested to review all details carefully and obtain expert professional advice with regard to specific legal, tax, and financial implications of the investment before making any decision relating to the purchase or sale of security in the Stock Market”.

Amanullah Khan, CFA

Assistant Manager

Strategy, Products & Data Science

Government of Pakistan Ijarah Sukuk (GIS) has seen significant progress in its issuance and accessibility since the shift of its primary market auctions to the Pakistan Stock Exchange (PSX) in December 2023. This transition to the capital market infrastructure has broadened participation, improved transparency, and streamlined the auction process through provision of a robust, in-house digital auction system developed by PSX.

GIS are Shariah-compliant financial certificates representing ownership in tangible assets, usufructs, or services. Unlike conventional bonds, GIS provide returns based on asset rentals rather than interest, making them compatible with Islamic principles. The Government issues primarily Ijarah Sukuk based on lease contracts, offering investors an ethical and Shariah-compliant investment option. The launch of GIS auctions at PSX marked a historic shift, enabling greater transparency, efficient price discovery, and wider market access. Investors can submit competitive bids, specifying the desired rental rate or spread - or non-competitive bids, accepting the rate set by the market. GIS offers stable, low-risk returns through fixed or variable rental payments, with tenors of 1, 3, 5, and 10 years. The minimum investment requirement of PKR 5,000 enables accessibility to a wide investor base, including individuals, non-resident Pakistanis (via Roshan Digital Accounts), and foreign investors. Investors can participate in primary market auctions and can also trade GIS in the secondary market via any Bills and Bonds (BnB) enabled broker (https://www.psx.com.pk/psx/themes/psx/uploads/List-of-BnB-Enabled-Brokers.pdf) .

Since the introduction of GIS on the PSX platform, primary market issuance has reached approximately PKR 3 trillion, while secondary market trading has surpassed PKR 600 billion. The primary market auctions have consistently witnessed an average oversubscription of 3.91 times, indicating strong investor interest. Retail investors can participate in these auctions through registered brokerage firms or online trading platforms, with detailed procedures available on PSX’s website.

A significant milestone for PSX and by association Pakistan, was the launch of the first-ever Green Sukuk at PSX, which successfully raised PKR 31.99 billion. The proceeds from this issuance are dedicated to funding environmentally sustainable projects, including renewable energy and climate resilience initiatives. This Green Sukuk aligns Pakistan’s capital markets with global Environmental, Social, and Governance (ESG) standards and highlights the growing global ESG Sukuk market, where Islamic financial instruments are increasingly used to support green investments worldwide.

Looking ahead, the GIS program aims to introduce additional tenors and expand Islamic financing structures, including Bai Muajjal Sukuk. Efforts are also underway to enhance retail investor participation through improved digital platforms and awareness initiatives. These developments reflect Pakistan’s commitment to expanding Islamic finance while integrating with modern capital market infrastructure. GIS represents a major step forward in aligning Islamic finance with contemporary capital markets. For investors seeking a Shariah-compliant, low-risk, and transparent option, it provides a credible and well-structured solution. Information on upcoming auctions, primary market data, and secondary market trading is available at www.psx.com.pk and www.dps.psx.com.pk

Amanullah Khan, CFA

Assistant Manager

Strategy, Products & Data Science

The Rise of ETFs: A Global Investment Revolution

The global financial landscape has undergone a profound transformation over the past few decades, driven by the emergence and widespread adoption of Exchange-Traded Funds (ETFs). These investment vehicles have reshaped how individuals and institutions allocate capital, offering a low-cost, transparent, and efficient alternative to traditional mutual funds. Assets invested in global ETFs have almost reached $17 trillion1, with more than 14,5001 ETFs trading on major exchanges, thus making ETFs a cornerstone of modern investing.

A Brief History: From Concept to Global Phenomenon

The idea of pooled investments dates back to the launch of the Qualidex Fund2 in 1970, the first open-end index mutual fund available to retail investors, designed to track the Dow Jones Industrial Average index. In 1975, Vanguard2 introduced the S&P 500 Index Fund, a landmark in making passive investing mainstream. ETFs are another form of pooled investment vehicle. The first ETF was launched in the Canadian market in 19902 to track the return of 35 large stocks listed on the Toronto resonating with a broad base of Shariah- compliant investors. As of now, nine ETFs are listed on the exchange, covering equity, debt, sector-specific, and Shariah-compliant strategies.

Current Landscape and Market Dynamics

While ETFs currently represent only a modest market share of Pakistan’s investment industry, interest is surging especially among first-time retail investors. With over 50% of listed companies being Shariah-compliant and almost 75% of trading value dominated by these stocks, the environment is ideal for passive investment vehicles like ETFs.

Improved macroeconomic indicators such as declining policy rates, a current account surplus, and an S&P sovereign rating upgrade have also contributed to a more attractive investment climate.

Strong Returns and Outperformance

In recent years, ETFs have frequently outperformed the broader PSX indices:

Best Practices for New ETF Investors

For newcomers to ETFs in Pakistan, it’s important to understand the underlying ETF strategy and fees structure before investing. Avoid speculative trading and consider ETFs as tools for long-term goals. Unlike mutual funds, ETFs disclose their underlying constituents daily which provides transparency and trade throughout the day. Dividends are typically paid as bonus units or cash, with at least 90% of income distributed to investors. Additionally, some ETFs trade on the futures counter, offering unique return opportunities for those seeking diversified exposure.

Conclusion: ETFs Are Reshaping Pakistan’s Investment Future

ETFs are not just another financial product, they represent a paradigm shift in how Pakistanis save, invest, and participate in economic progress. With cost-effective, transparent, and diversified exposure now within reach of every investor, ETFs are poised to play a transformative role in Pakistan’s capital markets.

As the ecosystem matures with improved infrastructure, cross-border partnerships, and investor education, ETFs will become a mainstay in retail and institutional portfolios alike.

Muhammad Hamza Khan

Assistant Manager

Strategy, Products & Data Science

Stock Exchange. However, the real turning point came in 1993, when SPY, the first U.S.-listed ETF was launched in partnership with S&P and the American Stock Exchange. SPY allowed investors to buy and sell an entire index like a stock, revolutionizing access to diversified investing.

Following SPY’s success, ETFs expanded rapidly across global markets, including Canada, Europe, and Asia. Over time, innovations like thematic ETFs, ESG-compliant ETFs, and actively managed ETFs further diversified the landscape.

Pakistan’s ETF Journey: First Listings and Market Entry

Pakistan entered the ETF space in March 2020 with the listing of its first two ETFs on the Pakistan Stock Exchange (PSX), the UBL Pakistan Enterprise ETF (UBLPETF) and the NIT Pakistan Gateway ETF (NITGETF). These launches marked a pivotal shift in a market traditionally dominated by bank deposits, national savings schemes, and actively managed mutual funds.

Later in the same year, the Meezan Pakistan ETF (MZNPETF) was introduced, offering a Shariah-compliant investment avenue.

Trading Activity and Liquidity

ETFs like JSGBETF, MIIETF, and JSMFETF depict healthy trading activity, averaging PKR 3 to 4.5 million daily since inception. MIIETF, notably, maintained 100% active trading days, suggesting increasing investor confidence and consistent market activity. While equity ETFs dominate, debt-based products are slowly gaining traction and represent future expansion opportunities.

Education, Inclusion, and Cross-Border Potential

Programs like “PSX Battle of the Bulls”, ETF trading simulations, Urdu-language resources, and PSX/SECP webinars have played a crucial role in educating young investors. These initiatives have led to notable increases in trading volume and participation, particularly from digitally engaged users.

With a robust ETF ecosystem, multiple fund managers, market makers, and enabling regulations, Pakistan is a strong candidate for cross-listed ETFs with other Asian markets.

Future Outlook and Strategic Opportunities The government’s “Uraan Pakistan” strategy prioritizes sectors like green energy, fintech, and digital infrastructure which are ideal candidates for thematic ETFs. Launching Shariah-compliant startup ETFs, ESG-aligned funds, or impact investment vehicles could unlock new sources of capital.

Technological innovation is enhancing ETF accessibility through robo-advisors and mobile-first apps. ETFs are evolving to align with ESG trends and national goals. Actively managed ETFs, popular globally, offer potential for alpha and volatility.

Magna Rohera

Assistant Manager

Strategy, Products & Data Science

Once upon a time in the bustling heart of Karachi, a curious 25-year-old named Ali arrived from a rural village, chasing a future shaped by ambition, hard work, and determination. He had always been captivated by tales of self-made individuals who transformed their lives not just with sweat and grit, but with clever choices and financial foresight.

One evening, while lounging at a friend’s place, Ali’s eyes fell upon an old, dusty book nestled on the coffee table. Inside were stories of legendary investors who had transformed their lives and the world through the power of saving and strategic investing. That moment lit a fire inside him, it was time to begin his own investment journey.

The First Lesson: Understanding Why Saving and Investing Matter

Ali reached out to Faizan, a close friend and seasoned investor who had weathered economic ups and downs with wisdom and resilience. Sensing Ali’s curiosity, Faizan happily assumed the role of a mentor.

Their first conversation was like opening the door to a new world. Faizan began with a stark reality: ‘Time and money,’ he said, ‘are the two currencies of life. Waste either, and you’ll pay the price.’

He spoke of the 2008 global financial crisis and the COVID-19 pandemic, both of which left millions jobless, businesses bankrupt, and families financially vulnerable. The lesson? Savings are one’s shield in chaos, and investments are their ladder to climb out of it.

The First Step: Budgeting for Freedom Before investing in stocks, bonds or any other investment avenue, Faizan emphasized budgeting as the starting point: ‘A budget is your money’s GPS,’ he quipped. ‘It directs where your money should go instead of wondering where it disappeared.’

He introduced Ali to the 50/30/20 rule:

This simple framework helps maintain discipline which is very essential on the road to financial freedom. ‘Discipline brings liberty,’ Faizan added. ‘It frees you from debt, anxiety, and the chaos of unpredictability.’

Setting Clear Financial Goals

With a budget in place, Faizan urged Ali to define his financial goals. These should span:

‘Goals give your money a purpose,’ Faizan emphasized. ‘Without them, income tends to vanish without a trace.’

Realities in Pakistan: Why Every Family Needs a Financial Plan

Faizan explained how Pakistan’s evolving family structures; from joint to nuclear households bring new financial responsibilities. Rising costs of living make emergency funds and insurance crucial.

He also highlighted the lack of retirement planning: over 65 million Pakistani workers are not enrolled in pension schemes, leaving many vulnerable in old age1. The reasons? Low financial literacy and lack of awareness.

‘As life expectancy increases and family support weakens,’ Faizan said, ‘planning for retirement is no longer optional, it’s essential for dignity and independence.’

Ali was surprised to learn Pakistan’s national saving rate is only about 7%2, much lower than neighboring countries. Faizan stressed that fostering a culture of savings and investment is critical not just for individuals but for the nation’s economic resilience.

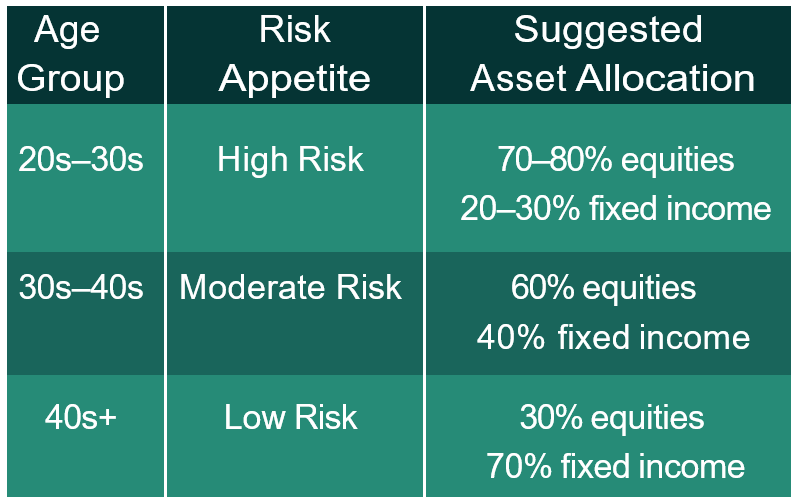

He also introduced the life-cycle investing strategy tailored to age and risk:

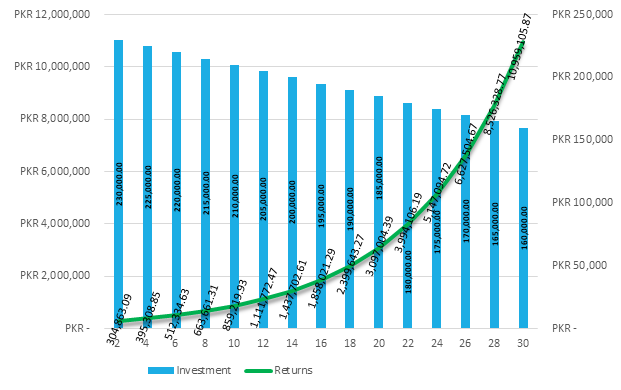

‘Start early to harness the power of compounding,’ Faizan advised. ‘The longer your money grows, the greater your wealth.’

Factors to Consider for Sound Investment Decisions

Before diving in, Faizan urged Ali to consider:

Navigating the Stock Market in Pakistan With Ali now convinced of the importance of saving and investing, Faizan took the next step and guided him through the process of opening a brokerage account to start trading at PSX:

Since Ali wanted to start with small investment, Faizan recommended opening a Sahulat Account which is a simplified account that only requires a valid CNIC, and allows investment up to PKR 1 million. Faizan also shared that many brokerage houses now offer online account opening, making the process faster and more convenient. The list of brokers with online services is available at ‘https://www.psx.com.pk/psx/online-accounts-opening’ .

Making Smart Investment Decisions

‘Ali, if you’re thinking of entering the stock market, do it wisely,’ Faizan said. ‘Consult registered brokers and aim for medium to long-term i.e. 3 to 10 years. Invest savings you won’t need soon, and diversify your money across different sectors that are not correlated.’

He leaned forward, lowering his voice. ‘Don’t fall for hearsay or hype. Research reports from brokers can really sharpen your judgment. Don’t invest all your savings, and definitely don’t chase short-term gains or unrealistic returns.’

Faizan paused, then added, ‘When picking stocks, check the company’s financial performance and future prospects. And always consider macroeconomic indicators like interest rates, inflation as well as geopolitics and industry dynamics, as these can turn market upside down.’

Overwhelmed by Stocks? ETFs Can Help

Ali was nervous about choosing individual stocks. Faizan suggested Exchange Traded Funds (ETFs) as a beginner-friendly way to invest broadly without picking individual stocks. He further explained that ETFs are baskets of stocks or bonds which trade on the stock exchange like individual stocks.

Currently, nine ETFs are listed at PSX, covering equity, debt, sector-specific, and Shariah-compliant strategies.

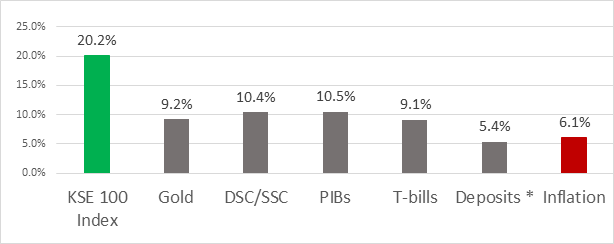

Here’s how the ETFs listed at PSX have performed since their inceptions:

Final Words of Wisdom

Faizan’s parting advice to Ali was simple but profound:

‘Investing is a journey. Start small, stay consistent, and let compounding work for you over time. Remember Warren Buffett’s wisdom, do not save what is left after spending, but spend what is left after saving.’ Empowered with new knowledge and a clear plan, Ali was ready to turn his dreams into reality, one smart financial decision at a time.

Climate change poses one of the greatest global challenges today, calling for innovative financial solutions. In the developing world, especially within the Islamic community, there is a rising demand for instruments that are both environmentally sustainable and Shariah-compliant. Green Sukuk offers such a solution—a Shariah-compliant bond crafted to fund eco-friendly projects.

To grasp the significance of Green Sukuk, we must first understand sukuk. Sukuk is an Islamic financial product, a Shariah compliant alternative to a conventional bond, based on Islamic principles. Unlike traditional bonds that pay interest - which is prohibited in Islam as “riba” - sukuk works differently. The issuer sells certificates to investors, using the funds to invest in tangible assets, such as infrastructure or property, in which investors gain partial ownership. The issuer promises to buy back these certificates at their original value after a set period, linking returns to the asset’s income in the form of rental and ensuring adherence to Islamic principles.

Since its introduction in Malaysia in 2000, followed by Bahrain in 2001, sukuk has gained global traction. Today, Islamic firms and governments widely use sukuk, contributing significantly to the international fixed-income market. By tying investments to tangible assets, sukuk aligns with Islamic financial ethics, offering investors ownership stakes rather than debt claims.

Green Sukuk takes this concept further, directing Islamic investments into renewable energy and other environmentally focused projects. It reflects Shariah’s emphasis on environmental care, with funds used for initiatives like building solar plants, retiring construction debt, or supporting green subsidies approved by the government. Often, it involves securing future income from specific eco-friendly assets or projects.

The global green bond market has surged in recent years, and Islamic finance is well-positioned to tap into this trend. This growth shows how capital markets worldwide are prioritizing climate considerations, a movement mirrored in Islamic finance through Green Sukuk issuances, including sovereign Green Sukuk. Case studies from various countries highlight how sukuk finances certified green projects, revealing enabling factors, challenges, solutions, and valuable lessons learned.

Pakistan is among the world’s most climate-vulnerable nations, despite contributing less than 1% to global carbon emissions. The country faces frequent climate challenges; floods, droughts, heatwaves and long-term risks like glacial melt and water scarcity. The 2022 floods, which displaced millions and caused billions of dollars in losses, highlight the urgent need for climate-resilient infrastructure. Green Sukuk provides a powerful tool to meet this need.

By raising funds for large-scale projects like dams, flood walls, and renewable energy, Green Sukuk helps Pakistan reduce reliance on conventional debt. It offers a sustainable way to address energy shortages and reduce dependence on imported fossil fuels. Shifting to clean energy sources such as solar, wind, and hydropower through Green Sukuk can cut energy costs and lessen environmental harm.

Pakistan’s thriving Islamic finance sector makes it an ideal candidate to leverage Green Sukuk, attracting investments from Islamic banks, sovereign wealth funds, and global ESG-focused investors who prioritize ethical, green projects. This not only boosts Pakistan’s global financial standing but also positions Islamic finance as a leader in sustainability.

Green Sukuk aligns with the Maqasid al-Shariah, the core objectives of Islamic law, which include preserving life, property, and the environment. It promotes sustainable development, environmental stewardship (khalifah), and the principle of avoiding harm (dharar), as noted in the World Bank Report. By offering a Shariah-compliant way to access global capital markets, Green Sukuk enables Islamic countries to uphold their values while pursuing sustainable growth.

Countries like Malaysia, Indonesia, Saudi Arabia, and the United Arab Emirates have successfully issued Green Sukuk, funding projects from clean energy to reforestation. By embracing this instrument, the Islamic world can lead in ethical and green finance, blending financial innovation with moral responsibility. This approach supports the United Nations Sustainable Development Goals (SDGs), establishing Islamic finance as a key player in global sustainability.

As major economies adopt sustainable business practices, Pakistan is recognizing the potential of sustainable investing. This approach integrates Environmental, Social, and Governance (ESG) factors into investment decisions, offering long-term financial benefits while tackling pressing issues like climate change, gender inequality, and socio-economic development. For a country facing both challenges and opportunities, sustainable investing is not just a strategy but a necessity.

With a young, growing population, rapid urbanization, and significant infrastructure needs, Pakistan requires capital to create jobs, reduce inequality, and drive clean, resilient growth. The Global Climate Risk Index ranks Pakistan among the top climate-affected nations, with floods, rising temperatures, droughts, and air pollution threatening agriculture, health, and the economy. Social challenges - gender inequality, poor education, youth unemployment, and limited healthcare - further hinder inclusive growth, while weak governance affects transparency and investor trust.

Sustainable investing bridges the government’s development goals with the financial market. By channeling capital into ESG-compliant projects, Pakistan can foster sustainable businesses, promote climate action, and build a more inclusive economy. In countries like Malaysia and Indonesia, capital markets are providing affordable, long-term financing through green bonds, supporting cities, municipalities, and low-carbon infrastructure. Pakistan, with its robust Islamic finance platform, can develop Shariah-compliant instruments that also prioritize sustainability, funding clean energy, social housing, and infrastructure while meeting both faith-based and ESG standards.

Marking a significant step in its sustainable finance journey, the Government of Pakistan has launched its first domestic Green Sukuk with a target issuance size of PKR 30 billion. This issuance will occur through an auction process, with the Pakistan Stock Exchange (PSX) - along with its infrastructure partners NCCPL and CDC - playing a key role in listing and promoting this innovative instrument. This move will transform Pakistan’s sukuk market by directing investments into eco-friendly projects, boosting economic growth, and aligning with international green financing standards. It reflects the government’s firm commitment to sustainable development through financial markets.

Green Sukuk highlights Pakistan’s dedication to lowering its carbon footprint while providing investors with a chance to support green initiatives. It represents a unique blend of faith, finance, and sustainability, enabling Pakistan to fund climate-resilient and clean energy projects in a Shariah-compliant way. Individuals, small to mid-sized investors, and organizations interested in joining the Green Sukuk auction can participate through licensed brokerage houses of Pakistan Stock Exchange, making this opportunity accessible to a wide range of stakeholders.

Imagine this: Ayesha, a schoolteacher in Faisalabad, sips her morning tea while scrolling through her phone. She stumbles upon a news headline: “Pakistan Stock Exchange (PSX) soars 84% in 2024!” Intrigued, she wonders, Could I invest too? Isn’t the stock market only for the wealthy or experts? Later, she learns that over 75% of daily traded value on PSX comprises of Shariah-compliant stocks. “Wow,” she thinks, delighted, as she has always wanted her hard-earned money to grow in a Shariah-compliant way. Like many Pakistanis, Ayesha once thought investing was out of reach. But her journey into the stock market changed everything—and it could change yours too.

The stock market once seemed like a distant, complex world, reserved for financial wizards. But today, with digital tools and accessible information, anyone—teachers like Ayesha, young graduates, doctors, housewives or on job professionals—can unlock its potential. The Pakistan Stock Exchange (PSX), the country’s sole stock exchange formed by merging the Karachi, Lahore, and Islamabad exchanges, can be your gateway to building wealth.

So, what is the stock market? Picture a bustling marketplace where buyers and sellers trade shares—small pieces of publicly listed companies. When you buy a share, you own a fraction of that company, whether it’s a bank, an energy firm, or a consumer goods giant. As a shareholder, you may earn dividends (a share of profits) or capital gains if the share price rises. For those seeking Shariah-compliant investments, PSX offers options like the KMI-30 and KMI All Share Islamic indices, which contains those companies that align with Islamic finance principles. It is worth mentioning that more than 50% of the companies listed at PSX are Shariah-compliant.

Ayesha’s First Steps: Starting Small, Dreaming Big - Ayesha was cautious. “What if I lose everything?” she worried. But she learned that the stock market offers unique advantages over traditional savings like fixed deposits or real estate:

To start, Ayesha opened a Sahulat Account with a licensed PSX broker, requiring only her CNIC. She began with a small sum, focusing on “blue-chip” stocks (shares of stable, profitable and well-established companies). She also explored Exchange Traded Funds (ETFs), which bundle multiple stocks for instant diversification, perfect for beginners wary of market swings. She also explored the option to buy Sukuk (Shariah-compliant debt instruments issued by the government) offering stable returns and aligning with her ethical values.

Learning the Ropes: Knowledge is Power - Ayesha didn’t dive in blindly. She explored PSX’s free resources to build her confidence:

She set clear goals: save for her daughter’s education and build a retirement nest egg. Ayesha learned to take a long-term view, resisting the temptation to chase quick profits. “The stock market rewards patience,” her broker advised. She diversified her portfolio, mixing defensive stocks (like utilities) with growth stocks (like tech firms), and even picked dividend-paying stocks for steady income.

Navigating Risks: Ayesha’s Smart Moves - The stock market isn’t a guaranteed win. Ayesha faced risks but learned to manage them:

Smart and prudent, Ayesha didn’t invest all her savings. She set aside an emergency fund for unexpected needs and allocated only the remaining funds for long-term investments, knowing the stock market tends to yield higher returns over time. By carefully managing her risks, she ensured her investments aligned with her financial goals and risk tolerance.

Ayesha stayed informed, following local news, policies from the State Bank of Pakistan and global trends like trade wars. She reinvested her dividends, harnessing the power of compounding to grow her wealth over time Ayesha stayed informed, following local news, policies from the State Bank of Pakistan and global trends like trade wars. She reinvested her dividends, harnessing the power of compounding to grow her wealth over time.

The Bigger Picture: Trust and Transparency - The Securities and Exchange Commission of Pakistan (SECP) regulates PSX, ensuring transparency and protecting investors. Ayesha chose a reputable broker from PSX’s approved list, avoiding schemes promising “quick riches.” She learned her rights as an investor through SECP guidelines, building trust in the system.

Ayesha’s Triumph: From Doubt to Confidence - Months later, Ayesha’s small investments grew steadily. Her portfolio wasn’t just numbers on a screen—it was a step toward her dreams. She wasn’t rich overnight, but she felt empowered, knowing her money was working for her. Whether saving for a house, an emergency fund, or retirement, the stock market offered endless possibilities.

Today, Ayesha is not only an active investor, she is also teaching her students basics of stock market. Ayesha knows that by investing in the stock market, not only she can achieve her financial goals but also contribute to Pakistan’s economic growth. When people invest in companies listed on PSX, they provide capital that fuels business expansion, job creation, and innovation. This strengthens industries like banking, energy, and technology, boosting the nation’s economy. A thriving stock market attracts foreign investment, stabilizes the rupee, and fosters sustainable development, creating a brighter future for all Pakistanis.

Your Turn to Start Your Journey - Ayesha’s story shows that the stock market isn’t a mystery—it’s a tool for anyone willing to learn. Start small, educate yourself with PSX’s free tools, and invest with discipline. Time is your greatest ally. With patience and calculated risks, the PSX may help you turn financial aspirations into reality. Open an account today, and take your first step toward prosperity.

Disclaimer: Investments in the Stock Market are subject to market risks. The prices of securities may go up or down depending upon the factors and forces affecting the securities market including but not limited to the fluctuations in the interest rates. Investors are requested to review all details carefully and obtain expert professional advice before making any decision relating to the purchase or sale of security in the Stock Market.

In today’s fast-evolving digital landscape, cybersecurity has become a top priority for financial institutions worldwide. As the backbone of Pakistan’s capital market, Pakistan Stock Exchange (PSX) is committed to maintaining the highest standards of information security, risk management, and operational resilience. In line with this commitment, we are proud to announce that PSX has successfully achieved ISO 27001:2022 certification, a globally recognized standard for Information Security Management Systems (ISMS).

This achievement underscores our unwavering dedication to protecting sensitive market data, investor information, and financial transactions from evolving cyber threats. It also reflects our proactive approach to regulatory compliance, risk mitigation, and business continuity, ensuring that PSX remains a secure, resilient, and globally credible financial marketplace.

Achieving ISO 27001:2022 certification was not an individual feat but the result of a concerted effort from all PSX departments. Every team within the organization—including Information security, Risk Management, IT, Operations, and Business Units—played a pivotal role in implementing strong security controls, governance frameworks, and risk mitigation strategies.

The certification process involved a rigorous assessment of PSX’s security policies, procedures, and technical controls, ensuring that they align with international best practices. By fostering a culture of collaboration and vigilance, we have established a security framework that meets global security standards.

ISO 27001:2022 is an internationally recognized information security standardthat provides a structured approach to identifying, managing, and mitigating security risks. Organizations that achieve this certification demonstrate their ability to safeguard sensitive information, maintain regulatory compliance, and uphold the trust of stakeholders and investors.

For PSX, this certification signifies:

1. Enhanced Data Security

It ensures confidentiality, integrity, and availability, and also strengthens data encryption, access controls, and threat detection mechanisms to safeguard critical assets.

2. Risk Mitigation and Cyber Resilience

It enables PSX to proactively identify vulnerabilities, implement preventive measures, and respond effectively to security incidents. This minimizes the risk of data breaches, unauthorized access, and cyberattacks.

3. Increased Stakeholder Confidence

Security is a key factor in maintaining trust among brokers, traders, investors, and regulatory authorities. By achieving ISO 27001:2022 certification, PSX provides stakeholders with the assurance that their financial and trading data is protected under globally recognized security frameworks.

4. Investor Trust and Market Stability

A secure stock exchange fosters investor confidence and market stability. Investors can trade with the assurance that PSX follows the highest security standards, reducing the risk of cyber incidents, and operational disruptions.

5. Global Credibility and Competitive Edge

Achieving ISO 27001:2022 enhances PSX’s reputation on the global stage. As the only Exchange in Pakistan, it is prudent to comply with international security best practices to attract global investors and market participants. This certification strengthens our position as a trusted exchange within the international financial ecosystem.

6. Business Continuity and Operational Resilience

PSX operates in a

fast-paced and high-volume trading environment

where downtime is not an option. The structured risk management framework of ISO 27001:2022 ensures that PSX remains operational even during cybersecurity incidents, technical failures, or unforeseen disruptions.

7. Regulatory Compliance and Legal Protection

The financial sector is subject to stringent regulatory requirements. Achieving ISO 27001:2022 certification ensures that PSX meets both local and international legal obligations, reducing the risk of non-compliance penalties and reputational damage.

While achieving ISO 27001:2022 certification is a significant milestone, it is not the final destination. Cyber threats are constantly evolving, and we recognize the need for continuous improvement in our security practices. PSX remains dedicated to:

This achievement would not have been possible without the hard work, dedication, and expertise of our Information security professionals, IT team, Risk team, and all PSX departments. Their efforts in implementing strong security controls, governance structures, and risk mitigation strategies have played a crucial role in securing this certification.

The successful achievement of ISO 27001:2022 certification reinforces PSX’s position as a leader in information security within Pakistan’s financial sector. As cyber threats grow in complexity, we remain committed to adapting, evolving, and strengthening our security frameworks to protect market integrity.

At PSX, security is not just a requirement—it is a core value that drives our operations and decision-making. This certification serves as a foundation for future innovations, enhanced risk management, and continued growth in the digital financial ecosystem.

Pakistan Stock Exchange is ready for the future—secure, resilient, and committed to excellence.

By: Babar Ahmed

Chief Information Security Officer (CISO)

Pakistan Stock Exchange (PSX)

Published On: March 15, 2025

The stock exchange plays a vital role in shaping a country’s economic landscape. In Pakistan, the Pakistan Stock Exchange (PSX) serves as the backbone of financial markets, providing businesses with access to capital and offering investors an opportunity to grow their wealth.

Despite its significance, a large portion of the general public remains unaware of the benefits of investing in stocks, limiting economic growth and individual financial prosperity.

Understanding the Role of the Stock Market in the Economy

A well-functioning stock exchange contributes to economic growth in multiple ways:

1. Capital Formation and Business Growth

The stock market allows companies to raise funds by issuing shares, enabling them to expand operations, innovate, and create employment opportunities. Successful businesses strengthen the economy by increasing productivity and tax revenues.

2. Wealth Creation for Investors

Investing in stocks offers individuals a chance to grow their savings. Over time, well-performing stocks yield significant returns, helping investors accumulate wealth and achieve financial stability.

3. Economic Stability and Development

A thriving stock market reflects investor confidence and economic stability. When the PSX performs well, it signals a robust economy, attracting foreign investments that fuel further growth.

4. Reducing Dependence on Foreign Loans

By encouraging local investment, the stock exchange reduces the need for foreign borrowing, which often comes with high-interest rates and economic dependencies. A stronger stock market means Pakistan can rely more on domestic resources for economic development.

Why the General Public Hesitates to Invest

Despite these advantages, many Pakistanis hesitate to invest in the stock market. Some of the key reasons include:

Encouraging Public Participation in the Stock Market

To make stock investment more accessible to the general public, the following steps can be taken:

Conclusion

The Pakistan Stock Exchange is a crucial driver of economic growth and financial empowerment. By bridging the knowledge gap and making investing more accessible, Pakistan can unlock the true potential of its stock market. Now is the time for the general public to step forward, learn about stock investments, and become active participants in shaping the country’s financial future.

Ahmed Chinoy H.I, S.I

Director Pakistan Stock Exchange Ltd

Published On: August 21, 2024

Pakistan Stock Exchange (PSX) presents a highly respected and prestigious award to highlight and celebrate the achievements of top 25 companies who have met certain qualitative and quantitative criteria in terms of their performance. The PSX Top 25 Companies Award is presented to listed companies who have excelled in both corporate governance and financial performance.

The Top 25 Companies Awards was established in 1978 and the very first award distribution ceremony was held in 1980. The objective of PSX Top 25 Companies Awards is not only to reward and recognise the listed companies meeting criteria of excellent performance, but also to set an example and benchmark for other listed companies to follow. At the same time, the award-winning companies are highlighted to local and global investors, given that these winning companies have achieved distinction on several grounds such as dividend payouts, capital efficiency and corporate governance metrics, to name a few of the factors against which these companies are selected. More recently, the selection criteria of SDGs and ESG related reporting as well as Diversity & Inclusion were also included in the Top 25 Companies Awards.

The PSX Top 25 Companies Awards is a touchstone for all companies to follow and achieve. The listed companies who win these awards are not only amongst the best performing companies in Pakistan but are also comparable to the best performing companies internationally.

Disclaimer:

The contents of this article/ blog comprising of information pertaining to financial products, including but not limited to securities, derivatives products, listed companies or companies proposed to be listed on PSX and any content of third parties are strictly of a general nature and are provided for informative and educational purposes only. Such content/ information is not intended to provide trading or investment advice of any form or kind and shall not under any circumstances be construed as providing any recommendation, opinion or indication by PSX as to the merits of the said product, security or company and also not be interpreted as comprehensive and interpretive of all applicable regulatory provisions

Published On: August 21, 2024

Pakistan Stock Exchange regularly holds Investor Awareness Sessions for the general public including students, academics/ faculty members of universities and colleges, corporate employees, self-employed persons and others. PSX also holds sessions for women in order to promote financial empowerment and awareness amongst them. Furthermore, PSX holds the Investor Awareness Sessions for corporates and companies. These sessions are useful implements to foster financial literacy and education amongst the general public and employees of companies. They are held through in-person or online platforms.

The Investor Awareness Sessions also align with the ‘S’ element of Environmental, Social and Governance considerations. These sessions help promote financial awareness in the society as a whole, and individuals in particular. As a frontline regulator, PSX proactively advocates ESG reporting and adherence. Pakistan Stock Exchange consistently takes steps to foster awareness on ESG for listed companies and stakeholders. As it stands today, companies that report on ESG are sought after by investors as responsible investment takes center-stage globally.

The Investor Awareness Sessions constitute of basics of stock market investment and role of stock market in capital formation & building wealth. The sessions disseminate awareness about savings & investments, asset classes available for investment in Pakistan, ecosystem of the capital market and functioning of the Stock Exchange. The importance of financial planning and various functions & operations of the Stock Exchange are also explained to the participants. The participants are also briefed on ways to navigate PSX’s website & how to access different types of information available on the PSX Data Portal.

The audience profile of the sessions varies from students, employees of corporates & other organisations, self-employed persons, housewives to other members of the general public who can greatly benefit from these sessions. These sessions are held for educational institutions, corporate organisations, chambers of commerce and industries, professional bodies and associations, among others.

Pakistan Stock Exchange, as the frontline regulator and the flag-bearer of Pakistan’s capital markets, recognizes the significance and value of disseminating and fostering investor awareness and education. These sessions are a useful resource for everyone to benefit from by augmenting their financial knowledge. The sessions are mostly free of cost and are a sound contributor to increasing basic financial knowledge and understanding amongst the general public.

PSX understands well that it is through efforts like these that the public can be encouraged towards investing and building wealth for themselves, thereby creating greater opportunities for themselves and securing their future. As the financial well-being of the individuals takes center-stage, this will result in greater economic activity and growth for the country as well.

Disclaimer:

The contents of this article/ blog comprising of information pertaining to financial products, including but not limited to securities, derivatives products, listed companies or companies proposed to be listed on PSX and any content of third parties are strictly of a general nature and are provided for informative and educational purposes only. Such content/ information is not intended to provide trading or investment advice of any form or kind and shall not under any circumstances be construed as providing any recommendation, opinion or indication by PSX as to the merits of the said product, security or company and also not be interpreted as comprehensive and interpretive of all applicable regulatory provisions

Published On: August 21, 2024

When investing in the market subsequent to opening an account with a securities broker, investors must be cognizant of their rights regarding investment in the market. From account opening and maintenance, investment process and procedures, to different caveats regarding investment in the stock market, investors must be careful and ensure that their rights are protected. For example, investors must not invest based on any promise of a fixed return or guaranteed returns by a securities broker; furthermore, investors must not authorise any broker to transact on their behalf or carry out trades without explicit permission or authority by the investor.

Investor Complaints Process & Resolution:

In case of any complaints or trade related dispute, the customer may at first lodge a complaint with his/ her securities broker. If the matter is not resolved, the customer may lodge the complaint with the Regulatory Affairs Division (RAD) of PSX to get relief or compensation. The complaint may be lodged by submitting a prescribed Investors’ Complaint Form (available on PSX website) at investor.complaints@psx.com.pk once an investor files a complaint, PSX takes up the matter with the concerned securities broker and initiates the process of the complaint resolution initially through mediation.

Arbitration:

If the matter still stands unresolved, despite mediation, then Arbitration is employed in accordance with procedures prescribed under Chapter 18 of PSX Regulations. Arbitration is a process of dispute resolution whereby a customer can settle their disagreement with the broker efficiently outside the Court. Any party to the dispute, whether investors alleging mismanagement of their funds or securities brokers for recovery of debit amounts, may file for Arbitration through an application to RAD supported by relevant documentary evidences. If the disputed amount is above Rs 1,000,000, then the Arbitration is carried out by a panel comprising of industry experts, CEOs of brokerage houses, and representatives of PSX senior management staff. The Arbitration panel provides equal opportunity of hearing to all parties involved in the dispute. In case the disputed amount is less than Rs 1,000,000, then the sole arbitrator who may be one industry expert hears and decides on the dispute. A decision is made after significantly reviewing the entire matter from all angles. If any party to the dispute is dissatisfied with the Arbitration result, they may file an appeal with the PSX Chief Regulatory Officer (CRO) within 15 working days of the decision. Subsequently, an Appellate panel comprising of five arbitrators including industry experts and PSX senior management staff will hear and decide on the Arbitration decision against which the appeal is being made within 45 days of the receipt of the appeal.

Default by a Securities Broker:

In case of default by a securities broker, a customer wanting to lodge a complaint against the said securities broker in respect of claiming funds, can do so by contacting the PSX Regulatory Affairs Division (RAD). The process involves formation of a Default Committee by PSX for handling such matters, inviting claims against defaulting securities brokers through PSX website and advertisements in newspapers, appointment of auditor for verification of claims, and disbursement of available funds to approved claimants.

The approved claims of defaulter securities brokers are settled by PSX through liquidation of assets of the securities broker and through the Base Minimum Capital (BMC) maintained with the Exchange in accordance with Chapter 19 of PSX Regulations. If the customers’ claims admitted by the Exchange against a defaulted securities broker are more than the amount available out of sale proceeds of assets of such securities broker and through the BMC for satisfying such claims, then remaining amount shall be paid from Centralised Customers Protection Compensation Fund (CCPF), established by the Exchange with the sole mandate to compensate customers of a defaulter securities broker, up to a maximum of Rs 1,000,000/- per claimant, in accordance with Chapter 24 of PSX Regulations.

While there are comprehensive measures in place to protect investors by PSX as a frontline regulator, the saying that “prevention is better than cure” or “better be safe than sorry” is the most apt in this situation. Being careful and investing responsibly is the best guarantee that an investor can have in terms of protecting his/ her investment and assets.

Disclaimer:

The contents of this article/ blog comprising of information pertaining to financial products, including but not limited to securities, derivatives products, listed companies or companies proposed to be listed on PSX and any content of third parties are strictly of a general nature and are provided for informative and educational purposes only. Such content/ information is not intended to provide trading or investment advice of any form or kind and shall not under any circumstances be construed as providing any recommendation, opinion or indication by PSX as to the merits of the said product, security or company and also not be interpreted as comprehensive and interpretive of all applicable regulatory provisions

Published On: August 21, 2024

Pakistan Stock Exchange’s ‘My Portfolio’ is a dynamic, educational, real-time based virtual trading platform. This web-based trading platform is designed for students, employees, business persons, market enthusiasts and the general public who wish to learn more about and practice investing. It is an ideal tool enabling creation of different portfolios and seeing the results of investment strategies in the stock market. To put it briefly, users of this platform can learn about the commissions & deductions, stocks & their symbols, and dividends, among other aspects of investing on the stock market. Through this tool, participants will also learn about their portfolio dashboard, diversification, and gauge their profits and losses.

My Portfolio is a risk-free way to learn about investing in stocks, thereby engaging in this productive activity with no cost and in a safe way. Learn how to build a virtual portfolio of stocks and how to subsequently track it through the dashboard of My Portfolio. Here you can add on an existing portfolio, add a new portfolio, buy & sell shares, and track your portfolio position with ease. Following are some tips and guidelines on using My Portfolio.

To use My Portfolio, click on ‘My Portfolio’ on the menu bar at the top of the Data Portal. To begin, create an account & sign up by adding your basic information and set up a password.

Next, create your first portfolio. Add in the name of the portfolio, specify the cash amount you want to virtually deposit against your portfolio, the tracking date of the portfolio, and a brief description of the type of portfolio this is going to be, whether it’s a portfolio focused towards capital gain, dividend income or any other form as per your preferences.

Upon clicking on Create Portfolio, your portfolio will be created showing a dashboard with your cash position. Now you can start adding shares or stocks to your portfolio by clicking on Make A Trade.

For the Buy Transaction, enter the symbol name of your selected stock pick, transaction date through the drop-down calendar, the stock quantity to be purchased, as well as the share price. The share price can be entered manually or fetched automatically. Then enter the brokerage fee as per your preference.

After Submitting the Buy transaction, you are presented with your portfolio position. Here you are shown the portfolio dashboard, the portfolio trend, the breakdown or graphical presentation of your portfolio as well as a tabular display of your portfolio. Through Make A Trade, you can enter multiple buy transactions.

For the Sell transaction, select a symbol of your stock pick, the transaction date through the drop- down calendar date, and the stock quantity for sale. Next, enter the share price you want to sell the shares at and the brokerage commission.

After submitting the Sell Transaction, your portfolio position is again presented to you incorporating the latest position of your portfolio of shares. Here you can see the details of your portfolio in terms of today’s returns, total return or gain/ loss, market value of equities, cash balance as well as total portfolio value. The portfolio trend shows the daily return chart of your portfolio. It is updated at the close of each trading day. The pie chart on the right of the portfolio trend shows the distribution of your portfolio in terms of equities and sectors. At the bottom, you are shown your portfolio position in a tabular form, with the Summary displaying the quantity of shares, average cost, current price, gain/ loss and the weight of each holding in the portfolio. Through the Transaction History, you will be able to track your transaction history on different dates.

You can also create multiple portfolios in similar way and switch between your portfolios. My Portfolio is a comprehensive tool enabling you to participate in stock trading and investment with zero risk and zero loss possibility. It is an extremely useful tool designed to help you understand investing on the stock market in a complete and productive way.

The My Portfolio Contest was also held to promote investor awareness and education. The winning contestants were awarded attractive prizes while learning the ropes of investing on PSX. By participating in My Portfolio Contest, the contestants were able to learn about investing, building a portfolio and taking investment decisions. Moreover, they could learn about stock prices, stock symbols and much more.

The contest was a three-month long activity in which the users were allocated PKR 10 million virtual cash in their portfolio and, during the provided timeline, users were asked to invest and trade by buying and selling shares. The top performing portfolios, in the final analysis, were rewarded. The contest was focused on encouraging potential investors to explore the market, make the right decisions and learn from their mistakes without incurring any real cash losses.

You can learn more about My Portfolio by accessing the video tutorial available at the following PSX You Tube account link:

Disclaimer:

The contents of this article/ blog comprising of information pertaining to financial products, including but not limited to securities, derivatives products, listed companies or companies proposed to be listed on PSX and any content of third parties are strictly of a general nature and are provided for informative and educational purposes only. Such content/ information is not intended to provide trading or investment advice of any form or kind and shall not under any circumstances be construed as providing any recommendation, opinion or indication by PSX as to the merits of the said product, security or company and also not be interpreted as comprehensive and interpretive of all applicable regulatory provisions

Published On: August 21, 2024

For all investors investing in the capital market, it is extremely important that they know and understand their rights regarding investor protection and the rules & regulations thereof. At the outset, when a potential investor is to open a trading account with a securities broker, he/ she must ensure that the broker is a Trading Right Entitlement (TRE) Certificate Holder of Pakistan Stock Exchange and is licensed by the Securities & Exchange Commission of Pakistan (SECP). A customer can verify if a securities broker is a TRE Certificate holder by visiting the PSX website and verifying the registration details of the brokerage firm along with its registered office and branches.

Account Opening & Maintenance:

When opening an account, customers are advised to ensure that the Customer Relationship Form (CRF) or Sahulat Account Opening form containing the minimum Terms & Conditions (T&Cs) should be read, understood and signed by them. Infact, all relevant fields of the CRF must be properly filled out and irrelevant fields may be struck off. Moreover, the T&Cs, annexed to the CRF/ Sahulat Account Opening forms provided to account holders must be duly stamped, dated and signed by the Compliance Officer of the securities broker on each page.

Investors are advised to open accounts in their own name only and encouraged to operate their account themselves. Investors are encouraged to open CDC Investor Accounts for safer custody of their shares. In case they want to authorise someone else to transact on their behalf, then a relevant authorisation must be furnished in writing to the concerned securities broker whilst a copy of the authorisation may be maintained by the account holder. Account holders are further recommended to keep track of all alerts, emails, messages or documents sent to them in respect of their account by their securities broker, as well as CDC and NCCPL. Account holders must also sign and verify the correctness as well as completeness of their UIN Post Report and CDC Setup Report.

Orders & Confirmations:

In order to protect the assets of investors, there are certain guidelines and regulations outlined by PSX. Account holders holding an account with a brokerage firm must place orders in written form or through recorded lines when placing orders verbally. The brokerage firm, on its part, must provide Trade Confirmations to the customers after execution of each trade. Furthermore, they must provide quarterly statements of the trading account to their customers. Receipts of margin deposits or payments must be provided by the brokerage firms to their customers. Brokerage firms are also required to provide the mandatory tariff structure to their customers.

Investment Process Caveats:

Investors must not invest based on any promise of a fixed return or guaranteed returns by a securities broker. Investors must not authorise any broker to transact on their behalf or carry out trades without explicit permission or authority by the investor. Investors must not make investment decisions based on advice by unlicensed investment advisors or follow any investment advice by unauthorised/ unregistered persons on any unofficial or unregulated social media platform.

Disclaimer:

The contents of this article/ blog comprising of information pertaining to financial products, including but not limited to securities, derivatives products, listed companies or companies proposed to be listed on PSX and any content of third parties are strictly of a general nature and are provided for informative and educational purposes only. Such content/ information is not intended to provide trading or investment advice of any form or kind and shall not under any circumstances be construed as providing any recommendation, opinion or indication by PSX as to the merits of the said product, security or company and also not be interpreted as comprehensive and interpretive of all applicable regulatory provisions

Published On: August 21, 2024

Becoming a Trading Right Entitlement Certificate (TREC) Holder of PSX enables the holder to carry out trading of securities at Pakistan Stock Exchange (PSX). The TREC Holders or securities brokers have the advantage of trading for themselves or for their clients. Infact, holding a TRE Certificate enables a securities broker to have more than just the license to trade on PSX.

There are multiple advantages of becoming a PSX TREC Holder. Through this facility, a securities broker gets the opportunity to participate in the multibillion-rupee industry by focusing on corporate equity side as well as the retail brokerage side. The former is geared towards trading for corporate entities such as Asset Management Companies, banks, DFIs etc. and the latter is geared towards facilitating the individual customers such as High Net Worth Individuals and retail investors. TREC Holders can direct their clients to invest in multiple sectors or industries available in the market; from ETFs, Modarabas, mutual funds to futures contracts and others.

By investing and trading for corporate entities, a securities broker can build a strong corporate network which will enable him/ her to capture a share of the institutional market activity. This will enable a securities broker to earn higher revenue streams and liquidity. At present, a TREC Holder can earn 0.15% of transaction value per trade. A TREC Holder can also invest in technology and save money by providing that technology or application to retail clients for investing on the stock market by themselves. This will enable the retail investors to invest directly in the stock market without using the services of an individual securities broker.

Furthermore, TREC Holders can also build partnerships with corporate investors for business development which can add to their revenue streams. Moreover, for both retail and corporate clients, TREC Holders have the option of outsourcing their back-office settlement and other operational processes to a Professional Clearing Member (PCM).

Additionally, TREC Holders can become underwriter for Right Shares issue. They can also become agents for buy-back of shares. As per current rules and regulations, TREC Holders can also act as Advisors for companies wanting to list on the Growth Enterprise Market (GEM) Board of the Exchange, thereby playing their due role of contributing to the growth of the economy. TREC Holders can become market makers as well and can offer government and corporate bonds through the PSX platform.

As mentioned above, there are numerous advantages to becoming a PSX TREC Holder. TREC Holders not only facilitate investors, listing of companies, and market making activity but also contribute to the growth of economic activity in the country.

Disclaimer:

The contents of this article/ blog comprising of information pertaining to financial products, including but not limited to securities, derivatives products, listed companies or companies proposed to be listed on PSX and any content of third parties are strictly of a general nature and are provided for informative and educational purposes only. Such content/ information is not intended to provide trading or investment advice of any form or kind and shall not under any circumstances be construed as providing any recommendation, opinion or indication by PSX as to the merits of the said product, security or company and also not be interpreted as comprehensive and interpretive of all applicable regulatory provisions

Published On: April 01, 2024

Pakistan Stock Exchange (PSX) is the national stock exchange of Pakistan. It was established with the name of Karachi Stock Exchange (KSE) on September 18, 1947. It was incorporated on March 10, 1949, under the name of Karachi Stock Exchange (Guarantee) Limited as a company limited by Guarantee. In October 1970, a second stock exchange was established in Lahore by the name of Lahore Stock Exchange (LSE) to meet the stock trading or investment and listing needs of the provincial metropolis of Lahore and its surrounding region. Then in October 1989, a third stock exchange was established in Islamabad by the name of Islamabad Stock Exchange (ISE) to cater to the investors and companies of the northern parts of the country.

Originally, KSE was a small bourse having only five listed companies with a total paid-up capital of Rs 37 million. As the years passed and more companies got listed, the first Index constituting the companies on the bourse was formed. It was called the KSE 50 Index. Gradually, as the number of listed companies and trading activity increased, the need for a truly representative index was felt and the KSE 100 Index was formed on November 1, 1991. Other indices such as the KSE 30 Index and KMI 30 Index along with the recently added sectoral & ETF indices were also added, thus bringing a total of 16 indices on the Stock Exchange.

Stock Exchange is a marketplace to facilitate issuers to raise capital in the form of equity or debt. At the time of initial public offering, the companies make offers in primary market and get themselves listed. Thereafter, trading takes place in secondary market in those listed instruments by the investors through the brokers who are registered with the Stock Exchange as well as Securities & Exchange Commission of Pakistan (SECP). The companies listed on the stock exchange pay return to their shareholders/subscribers, in the form of dividend or mark-up/profit respectively on the investment made in equity or debt.

In the earlier days, trading of shares used to take place through open outcry on the trading floor. This was a traditional way of communication between stockbrokers where verbal communication and hand signals were used for conducting transactions. One stockbroker would communicate that he was interested to buy a stock while another stockbroker would communicate that he was interested in selling a stock. Hence a buy/sell deal was made across the trading pit. The open outcry method was eventually replaced in 2002 by the electronic trading system. The Karachi Automated Trading System (KATS) became operational at the Stock Exchange which was a robust, high performance and high capacity trading system. This was later replaced by the New Trading & Surveillance System (NTS), a cutting edge, future-ready, and robust trading system, which was successfully implemented, installed and adopted in 2023.

The three stock exchanges had separate management, trading interfaces, indices and no mutualized structure. In March 2012, the Stock Exchanges (Corporatisation, Demutualization, and Integration) Act 2012 was passed by the Parliament of Pakistan and in the month of May of the same year, it was signed by the President of Pakistan. By virtue of the said Act, all three stock exchanges were converted into companies limited by shares and it resulted into separation of ownership rights with the trading rights. The brokers were termed as initial shareholders who were issued shares of respective stock exchanges together with Trading Right Entitlement Certificates (TRECs). The said Act also required all the stock exchanges to divest 40% of their equity to strategic/anchor investors and 20% to general public.

In order to implement the condition of divestment of shares laid down in the above-referred Act in letter and spirit, it was felt to have only one stock exchange available for this purpose to the potential investors. As such, the operations of all three stock exchanges were ultimately integrated and a single entity with the name of Pakistan Stock Exchange Limited (PSX) emerged on January 11, 2016. It was followed by sale of 40% equity stake of PSX to Chinese consortium in the end of 2016 and offer of 20% equity stake to general public and self-listing of PSX in June, 2017. As such, PSX is now a commercial entity as well as an active frontline regulator of the capital market.

Many developments have taken place at PSX over the last few years. These include upgradation of PSX technology platform wherein a new Trading & Surveillance System has been implemented at the Exchange as mentioned above. Furthermore, the Exchange has brought forth new technological innovations and conventional developments such as the Online Account which allows investors to open an account digitally, the Sahulat Account which requires a simplified and convenient account opening process, the PSX WhatsApp Service to make available a whole host of information to users on their finger-tips, the My Portfolio virtual trading platform to enable users to learn the ropes of investing through real time trading but with virtual cash, the PSX Knowledge Center, which is a repository of articles, blogs and financial calculators related to the capital markets, and the PSX Glossary which consists of a list of 375 terms and definitions to enhance and increase knowledge on the financial markets. Over the past few years, nine Exchange Traded Funds have also been launched at the Exchange. These ETFs belong to different categories such as those of equities, debt and Islamic.

Ecosystem of the capital market of Pakistan

The ecosystem of the Capital Market constitutes different parts which together enable the working of the Market as a whole. This can be explained via the following diagram:

The companies at the forefront with PSX in the ecosystem of the Capital Market of Pakistan are Central Depository Company of Pakistan (CDC) and National Clearing Company of Pakistan Limited (NCCPL). CDC handles the transfer of shares traded and keep the custody of shares held by investors electronically while NCCPL provides clearing and settlement services of shares and funds against the transactions conducted at the Exchange.

PSX – the premier capital market of Pakistan

Pakistan Stock Exchange lists 524* companies on the Main Board and 3 companies on the GEM Board, representing 37 industrial sectors having a total market cap of over Rs 9.31 trillion. In recent past, PSX outperformed the stock markets of the region by becoming the best performing market in Asia and was also the proud winner of Best Islamic Stock Exchange Award for three consecutive years, 2021, 2022, 2023, presented by Global Islamic Finance Awards (GIFA).

Pakistan Stock Exchange plays a crucial role in the country’s economy as it channels domestic savings and foreign capital to the economic coffers of the country. By attracting interest from local and foreign investors, much needed capital inflows are channeled in the country through PSX. There are more than 313,000 investors investing on the Exchange. Pakistan Stock Exchange provides for an attractive avenue of investments with Price to Earning Ratio of 3.97, which is the lowest in the region and the MSCI Emerging Markets. This is a clear reflection of the attractive valuation of stock prices prevalent at PSX. Not only that, Pakistan Stock Exchange has provided the highest Dividend Yield of 9.38% as compared to other markets of the region and the MSCI Emerging Markets. Not only for investors, but also for companies, PSX is an attractive capital market. By listing on the Stock Exchange, companies can obtain much needed financing to fund their growth, invest in new projects, and increase the country’s exports. Companies listed on the Exchange provide employment and benefits to thousands of Pakistanis and their families and generate significant tax income for the Government of Pakistan.

Disclaimer:

The contents of this article comprising of information pertaining to financial products, including but not limited to securities, derivatives products, listed companies or companies proposed to be listed on PSX and any content of third parties are strictly of a general nature and are provided for informative and educational purposes only. Such content/ information is not intended to provide trading or investment advice of any form or kind and shall not under any circumstances be construed as providing any recommendation, opinion or indication by PSX as to the merits of the said product, security or company and also not be interpreted as comprehensive and interpretive of all applicable regulatory provisions

*(KSE 100 Index Annual Average Return for last 10 years - Feb 28, 2013-Feb 28, 2023)

Source:

Published On: October 01, 2023